Q. Please Introduce LoanMeet.

Loanmeet.com is a P2P Lending website. We are an online platform wherein we connect both the Borrowers and Lenders wherein the Borrowers have to pay a reasonable rate of interest and the Lenders earn more than the FD and Post Office Savings. For example when a person goes to put there money in an FD he would typically earn anywhere between 7-9% whereas the average return we provide is 18%. Similarly when a salaried individual applies for a Personal Loan we would typically be paying more than 24%.

The huge gap in the interest rate is the earnings of Banks and NBFC’s. We want to address this gap and have a win win situation for both the borrowers and the lenders.

Q. When and How did you think about loanmeet.com ?

The idea of LoanMeet came during a simple conversation with a fruit vendor. In Vadodara ( Gujarat ), Mr. Patel ( not the real name ) came everyday near my home, and sold fruits from footpath. I, Sunil Kumar – founder of LoanMeet, use to wave him ( say hello ) in the morning. On couple of occasions, I bought guavas from him. On one fine day, I spoke to him about his finances. He told me that he gets his guavas from a fruit wholesaler in the morning for roughly Rs. 200, and sells those for around Rs. 400. On most days, he makes around Rs. 200, and that money covers his daily expenses. He is poor, and he lives in slum.

Mr. Patel has an excellent business ( 100% profit on investment ); however, he still could not improve his daily living standards. Most of us would love to work in an industry where ROI ( return on investment ) is 100 %. Later, I went to a cookware retailer who wanted to open a wholesale store. I asked him to show his balance sheet and his projections. Later, I researched cookware industry and margins. Both he and I were confident that he could make his investment in an year. The bank wanted more than 130 % collateral in gold from him. He did not have that much gold. The bank guys were not willing to take his shop or his home as collateral.

My close friend wanted to buy a house near his office. He was able to get 15 % of loan amount for the down payment. The bank wanted 25 % for the down payment, and loan fees were roughly 1.5 % of the loan amount. He worked at a well known MNC, and he made good money, five times the EMI. However, since he just passed from college two years ago, he did not have enough money for the down payment. He felt frustrated, and gave up on his dream home. There are similar stories around us, and I hope you can relate to most of these stories.

On the other side, few of my friends have made good money ( more than a crore ) in real estate, and they are looking to invest their money. They like the idea of investing in stock market, but they do not have a good understanding of stock market and companies. They do not want to invest in gold, and then keep gold in lockers. Most of their money is parked in saving accounts. Some of them continue to invest in real estate. Lately, the prices of homes have steadied, and they want to pull money from real estate.

They feel uneasy about the whole process of giving money to family and friends. They are not sure whether they would get the entire principal amount from their friends or not. Will their friends ( borrowers ) pay them any interest ? Before giving money, can they trust the borrowers ? Is he/she going to spend the loan amount on something other the purpose of loan ? On the other hand, most individual lenders charge upwards of 25 % interest for personal and business loans. Some of them charge 40% interest on loans, and they would make money even if 30% of their borrowers default on their loans.

At LoanMeet, we plan to address these issues. We are building a platform that both borrower and lenders can trust. Before he list the loan, we run multiple checks on the borrower’s profile, and his loan request. If we see any red flags ( unusual spending patterns or incorrect answers ), we do not list the loan at our site. We want to provide the loans to needy individuals who are genuine and can return loan amount on time. Like banks, we do background checks, validate home address, study credit report, and get a loan guarantor. We go beyond regular financial institutions to protect lender’s investment.

For borrowers, we only need five set of documents to build your credit profile. If we need additional information, we might ask for additional documents. However, our process is quick, days not weeks or months. We rate all our borrowers, and then list their profile and loan details at our site. Please understand that the lender is investing in you because he put his trust in you and our platform. In case of default, we will approach collection agencies to collect the principal amount, interest, penalty, and late fees. If you intend to default, I suggest that you do not list your loan at our site. We do not take any bribe; we are here to enable individuals accomplish their dreams.

Most product owners claim that their products is useful to anyone and everyone. Well, we do not want to claim that. Our product, LoanMeet, is NOT suitable for folks who can raise money from their family members, as the interest rate on those loans is usually zero. As a lender, if you have never given money to anyone, then please start with a small amount at our site. Once we have earned your trust and confidence, then please invest more and spread the word. We want you to have a good night sleep, not worry too much about the money given to the borrower. As a borrower, if you plan to ask your father or close relative for money and you are 100% sure that you would get money, then there is no point in registering at LoanMeet. We are trying to solve lending and borrowing issue for 90 % of cases, where lenders go through sleepless nights after giving money and borrowers are unable to raise cash for their needs.

In simple words, LoanMeet provides peace of mind to lenders, and help borrowers quickly raise cash.

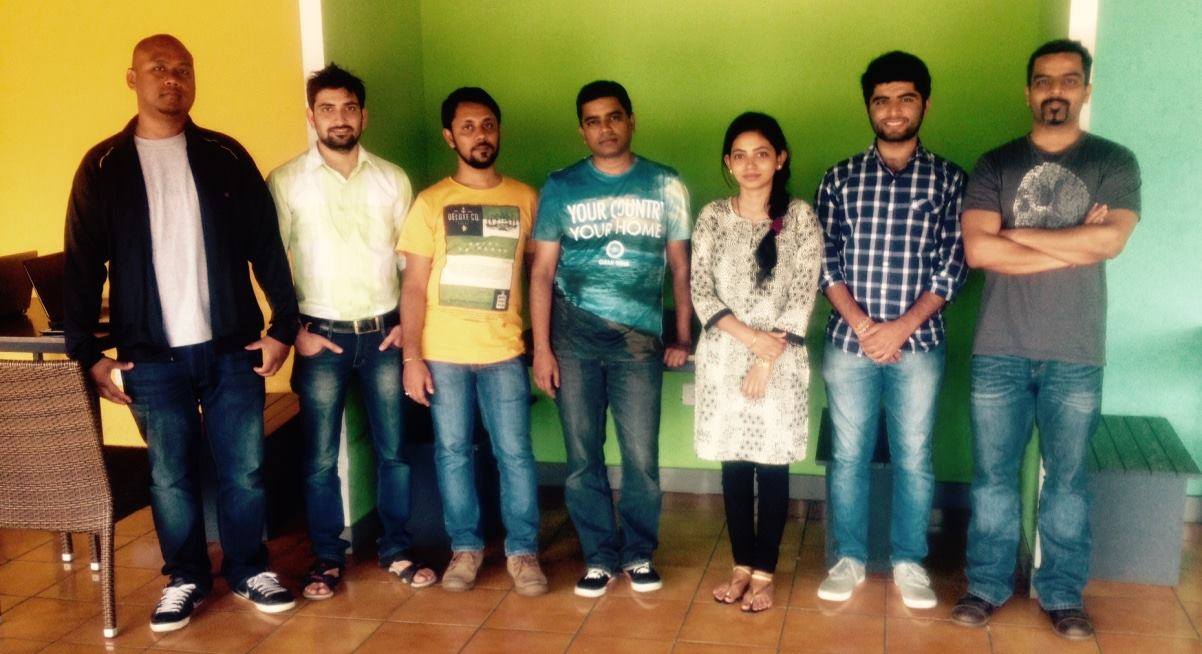

Q. Introduce your Co-Founders and Team.

Sunil kumar (Founder & CEO) : 2001 IIT Mumbai Graduate; MBA from Xavier University, Cincinnati, USA; 15 Years of Work Experience; Designed suspensions at Mercedes-Benz, and built IT Products at multiple companies; Built Risk Models at Federal Home Loan Bank. He is the one who has assembled our crazy bunch and transformed it into a superbly functioning team. A passionate leader. An awesome mentor. A workaholic. Had a beautiful life in United States but he thinks that personal financing in India needed an uplift as a vast majority of Indians still don’t have access to bank loans and are stuck with a non transparent, unfair lending system.

Ritesh Singh (CTO & Co-founder): VJTI CS Graduate; Sold one startup to ICICI Bank; Worked at CISCO; Built another startup. He is passionate about technology and a total coffeeholic. Loves having random conversation on machine learning, latest javascript framework or pretty much anything tech.

Vedant Bhotika (VP Business Development) : Veteran of Two startups; MBA from Welingkar. He handles operations and strategy as part of the broader initiative of Business Development.

Divya Naik (Relationship Management) : Fashionista, Photographer, and speaks half of Indian languages Before joining LoanMeet, she worked in HR department of one firm, and IT support department of another firm. She handles the customers from the first touch point to the last.

Pawas Pritam ( Credit Manager): MBA; Worked at Magma (NBFC); Worked at P2P Lending Startup. He takes care of the all the credit policies and approvals of the case’s at LoanMeet.

https://twitter.com/loanmeet/status/731038986307702784

Q. What makes you special and how is it different from others?

Loanmeet is different because it aims to solve the problem of how credit system functions. The basic difference between us and others is that we don’t discriminate customers on the basis of the salary drawn or the employer he is working for. Our target audience are those people who have very low salary or working at a SME. Our analysis of the sector tells us that people drawing low salary or working with a small company get there loans rejected or get very high interest rates to pay even though they might be having a CIBIL score on the higher side.

Q. What’s the Current Path and future plans?

We currently have 2300 active Borrowers and 463 active Lenders. We are currently expanding rapidly growth a rate of 30% MoM. Our business model stands validated as we have disbursed loans of 1.2cr till now. We hope to cross 3 cr by the end of this financial year.

In the end of the interview, Sunil shared these kind words about VID.

“VID is a great place to know about different types of startups and the difficulties that they faced. Some stories are really great and motivates to really get there and be the change.”

VID Team thank you for sharing your startup story, we wish you all the very best with your venture.